Observations from ALM Model Validations: Cost of Funds Back Testing

September 3, 2015

In the course of working with hundreds of credit unions and performing A/LM model validations, one area of weakness we see is in assumptions related to the cost of funds. Quite often, the modeled cost of funds does not (without good reason) represent historical costs as rates rise.

There are two major assumptions that influence cost of funds: Pricing strategy (betas) and deposit mix changes.

On the pricing, consider studying actual rates the credit union paid when rates were at 5% in the summer of 2007. If you are assuming the credit union won’t have to pay as much, why?

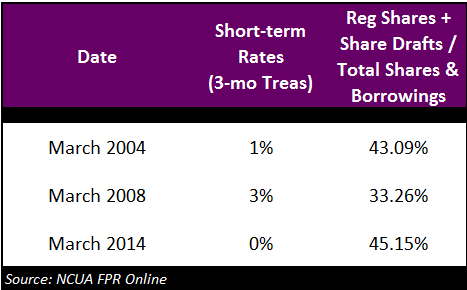

Another component to consider is the mix of funds as rates rise. The table below highlights how the distribution of funds is different in low and traditionally more “normal” rate environments.

Credit Unions $500M and Above

A good way to do a reasonableness check on the modeled cost of funds is to compare the total resulting cost of funds to the total cost of funds the credit union experienced historically, for example in 2007.

If the simulated cost of funds does not back test to history, you may be using a model that only applies decay assumptions to NEV and not the income simulation. This happens frequently.

Another reason could be that you are doing a static balance sheet simulation. Static balance sheet simulations ignore the risk of the deposit mix changing. This, of course, will water down the estimated cost of funds.

There can be supportable reasons why the cost of funds does not back test to history. However, we typically find that the simulation methodology used is driving this difference.