It’s Prime Time for Digital Lending – Leverage Data Insights

April 29, 2020

5 minute read – Digital channels have suddenly shot to the forefront for the ultimate test – are they ready to handle the lion’s share of volume efficiently while delivering outstanding customer experiences? Leadership teams are telling us that, while they have been steadily improving digital channels for years, COVID-19 has provided the impetus to quickly get positioned for a primarily digital world, and lending is a major focus.

Demand for consumer loans is almost at a standstill at the moment, and the longer-term forecast is uncertain. Looking back, the Great Recession taught us that winning a street fight for loans requires outstanding customer experiences and internal efficiencies. This time, the focus will be on outstanding experiences and internal efficiencies through the digital channel, because there is a good chance that consumers will prefer to conduct business remotely even after restrictions are lifted.

What the numbers are trying to tell you:

Taking a data-driven approach to understanding the digital channel experience helps hone in quickly on areas that need attention. Here are a few of the many data points that can provide insight that leads to action:

Few digital applications. Use of digital lending channels was already on the rise and is poised to go higher. If people are using digital lending, but your digital volumes are low, it’s critical to understand why – especially now.

A lack of traction for the digital lending channel can be caused by a poor experience with the app, ineffective marketing, and even employees that are incentivized to shift apps away from digital. Often, it is a pervasive branch-first mindset within the organization. Imagine that going forward, far more of your applicants will have today’s digital experience. Is it less than ideal? Common issues include:

- Applications that are too complicated or take too long

- Applications that are difficult to use on a mobile device

- Asking for more documentation than is absolutely necessary

- Confusing applications or instructions

Studying how many applications are abandoned and where in the process is highly informative.

Low approval rates. How do the approval rates for digital applications compare to branch or phone? Be sure to compare similar applications, such as used autos with B credit, across channels. If the approval percentage for digital applications is lower, it could be because:

- Underwriters view them differently

- Business rules are geared for in-person applications

- Slow or no follow-up by staff on applications with questions that must be answered before decisioning

- No champion to make the case for the customer like there is with branch applications

- Difficult communication

It can be harder to reach people who’ve applied via digital with follow-up questions. Reevaluate whether you really need to have the answers before making a decision. Also, are you making it easy to communicate with you via text, email, phone, and chat? If approvals are low because of unanswered questions, find out whether the follow-up for these applications is appropriately prioritized.

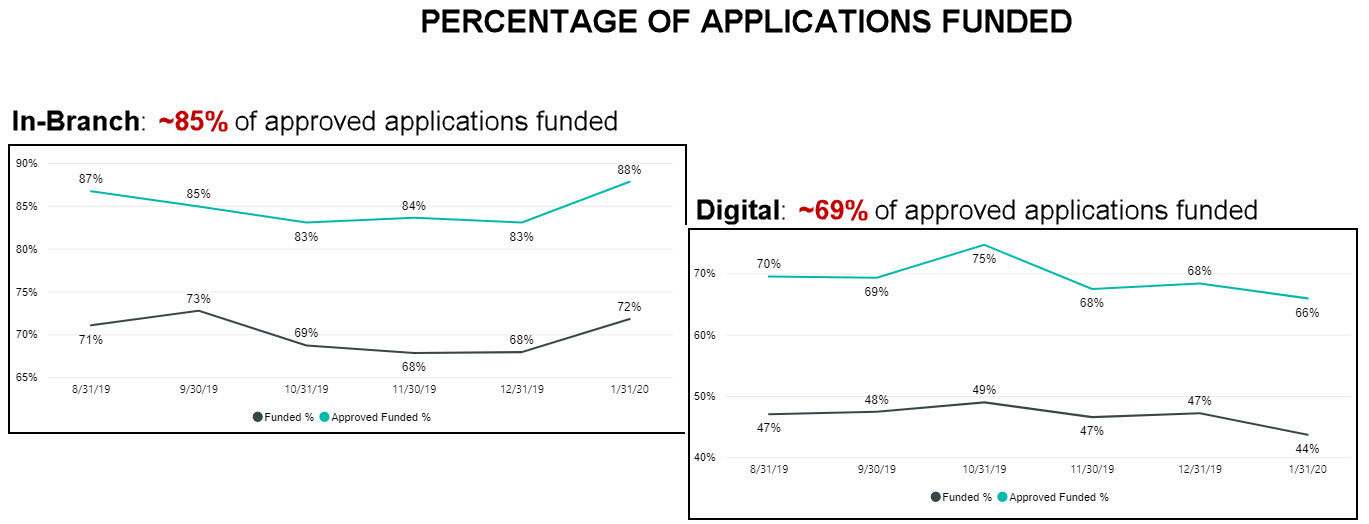

Low funding of approved loans. Compare the percentage of approved applications that are funded across channels. If fewer of the approved digital applications are ultimately funded, it could be due to:

- Slow response to the customer on the approval

- Vague communication

- Asking for too much documentation

- An unappealing offer

Use your data to see if the time it takes from when the application is submitted until a decision is made is slower for the digital channel. A slow decision combined with vague communication such as, “Thanks for your application. We’ll get back to you soon.” can cause your potential customer to move on to another lender.

Having to provide a lot of documentation can feel like jumping through hoops. Extra documentation may feel safer to the institution, but it must be weighed against the cost of lost loans. If you can’t approve what was asked for, make sure that counteroffers for digital applications are similar to other direct channels.

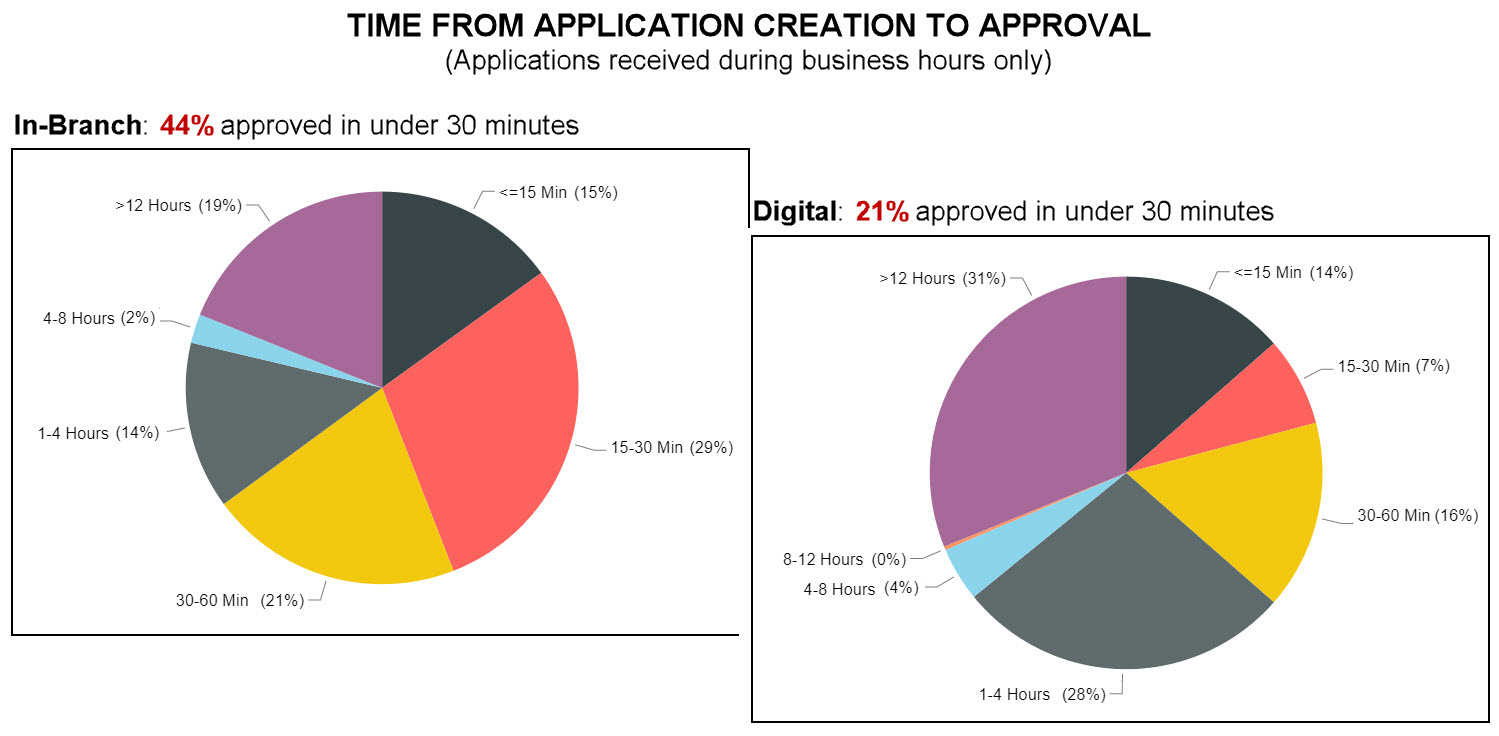

Automated decisioning. This capability is key for the digital channel, but what percentage of applications are actually auto-decisioned? If the number is low, invest the time to adjust parameters and parallel test. An instant decision eliminates the opening for your potential borrower to disengage and seek another lender while they wait to hear back from you. Beyond being good for the digital channel, auto-decisioning more applications for all channels frees up time that can be spent on the applications that need more effort.

Outside of business hours. Check funding rates for applications that come in outside of business hours. Separately, how many applications that won’t be looked at for a day or more are ultimately funded? Low funding percentages could indicate the need to get creative in order to respond faster.

To dig deeper to understand the performance of your digital lending channel, look at what the numbers are trying to tell you. They can lead you to ask the right questions to take digital lending to the next level. Then decide what steps you’re going to take. A new level of comfort with making decisions and taking action rapidly has come out of this crisis. Take this moment in time to become more successfully rooted in the digital world and ensure that your digital lending channel is positioned for the future.