New and Emerging Strategic Questions Surrounding Indirect Lending

March 6, 2019

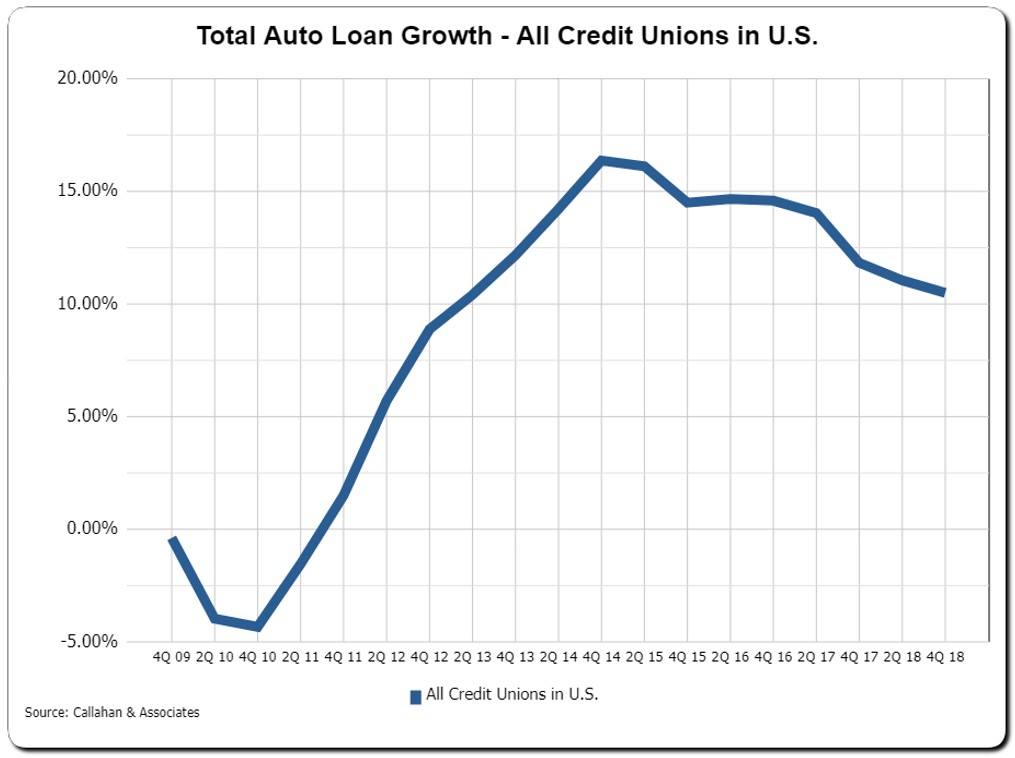

Higher auto rates, whispers of a potential recession, and rising prices of cars have made just a minor dent in recent credit union auto growth. While auto loan growth has been trending down, many credit unions continue to experience double digit auto growth.

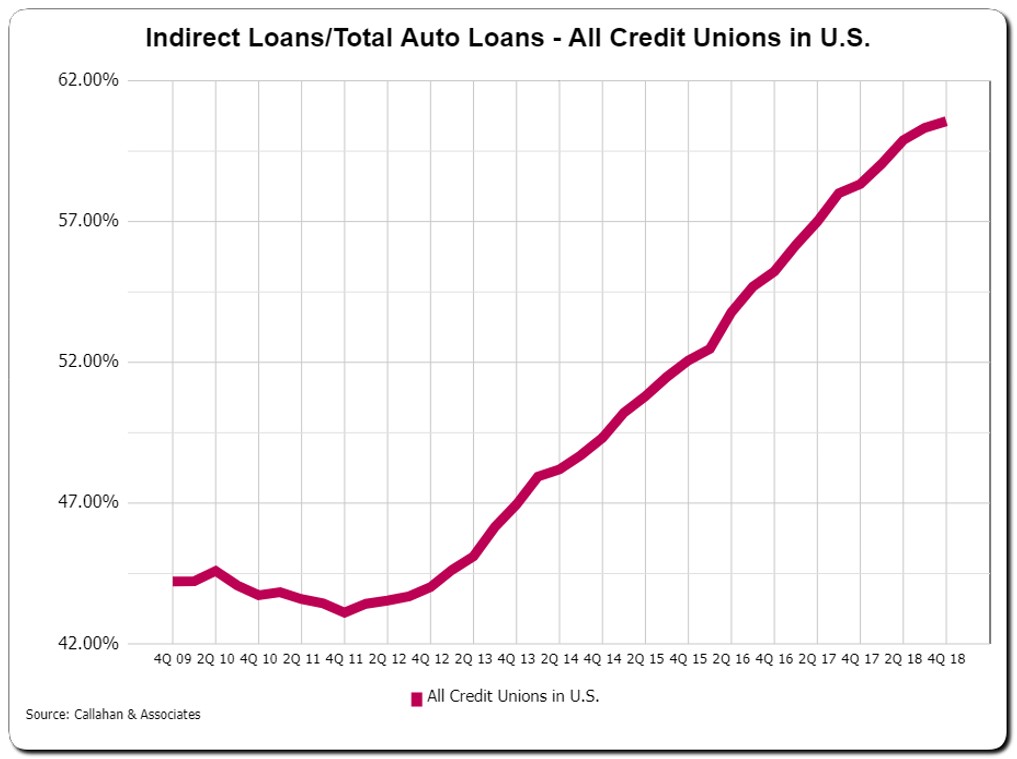

While the resiliency of auto sales continues to be an opportunity for many credit unions, it is important to understand the potential business implications of how auto growth is being achieved, which is primarily from the point of purchase (indirect) channel.

*Indirect loans includes all types of indirect loans. Autos are the primary driver.

As mentioned in a blog post from October 2017, growth in indirect loans and members is not necessarily a bad thing – in many ways, the growth can be positive if it is managed appropriately and the right questions are being asked.

While the strategic questions from the blog referenced earlier remain relevant, there is a growing sentiment from credit unions that the consumer or member has spoken in terms of how it wants to conduct business. Clearly there appears to be a desire for the convenience of point of purchase transactions and additional questions are rising to the surface.

- How many indirect loans are being made to existing members versus new members?

- If most of new member growth is coming from the indirect channel, what are intermediate- and longer-term business implications to consider? The most immediate things to consider are deposit acquisition and impact to non-interest income.

- Since it is clear that consumers value the indirect channel, how can credit unions more quickly leverage their digital delivery channels to satisfy consumers’ desire for ease and convenience and have opportunities to cross-sell other value-add products and services?

- As consumers’ preferences continue to evolve, how should decision-makers’ perspectives on concentration limits and other risk limits also evolve?

These thought-provoking questions are great scenarios to test drive with ALCO and/or management. Test driving the strategic implications and simulating possible financial outcomes can be extremely valuable to help inform timely adjustments that need to be made to optimize business models.