Strategic Budgeting/Forecasting Questions: Connecting The Strategy

This last entry in our 6 blog series about Strategic Budgeting/Forecasting Questions addresses creating a more thorough understanding of the connections between strategies and the budgeting/forecasting process.

Question 6 – What are other questions we should be asking?

While this may at first seem like an open-ended consideration, the goal of this question is to use a very specific approach to create more and deeper dialogue about the strategies and their reflection within the budgets and forecasts. Very literally, we recommend asking senior management, What other questions should we be asking? Using this approach can often bring to light those areas where concerns or obstacles may exist, creating a safe and collaborative opportunity to discuss them.

Some variations of this question may also be appropriate, such as, What are the unintended consequences of what we’re asking for? Or, Is there something in what we’re doing that is creating a barrier to being successful with our strategic initiatives?

Asking such questions may be uncomfortable at first because it invites differing points of view and increased scrutiny of what may be the greatest challenges facing the desired strategy. However, any initial discomfort is certainly worth the potential rewards—achieving greater buy-in and alignment with strategic directions and creating an opportunity to identify potential obstacles early.

Of course, inviting open dialogue does not equate to an obligation to change the given strategy. It simply better informs leaders about what may be ahead and allows the group to consider if any course changes might improve the opportunity for success.

For example, what if—through these questions—the board learned that the annual measure of success requiring the credit union to achieve a 1.00% ROA was getting in the way of being successful with the strategic initiative to remain relevant to the membership? The board may have anticipated that the relevancy initiative would come at some cost to the credit union, but may not have recognized that the previously agreed upon measures of success might hobble that goal. While a change could be made, it might also be an opportunity for the board to reiterate and clarify the reasons why the existing goals should continue without change.

The stakeholders have the same overall goals—a safe, sustainable, viable, and exciting organization to best serve the membership. Trusting in that can allow for deep and honest dialogue about the road ahead. As a final, solidifying step to ensure everyone is on the same page and has a clear vision of the expectations, credit union leadership can ask, What are other questions we should be asking? By so doing, senior management will be better prepared to follow through and deliver on the strategic initiatives reflected within the budget and financial forecasts.

In this blog series, we explored the critical role of connecting the dots between strategic initiatives and the budgeting/forecasting process. Specifically, we discussed the following questions:

- What is the expected financial direction of each strategic initiative?

- How are strategic initiatives represented in the budget and forecast?

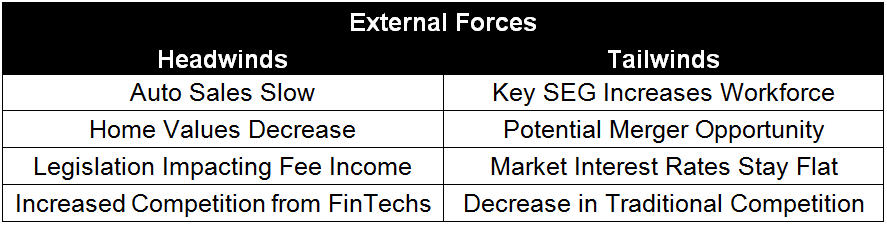

- What key forces could impact our forecast?

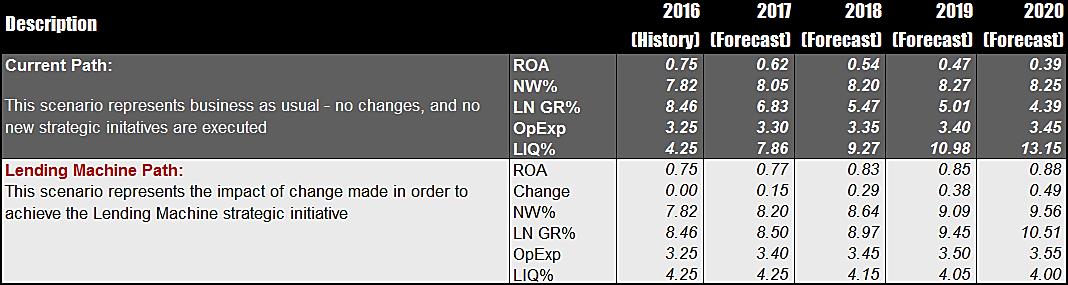

- Are our financial measures of success handcuffing the credit union strategically?

- How is the budget and forecasting linking to our appetite for risk?

- What are other questions we should be asking?