HELOCS May Be Set To Take OFF – Is Your Credit Union Ready?

July 25, 2018

For the last 10 years it seems like the home equity line of credit (HELOC) has been a forgotten product for many credit unions and their members. As rates on fixed mortgages hovered at record low levels, and with home equity under pressure, the demand for variable rate HELOCs decreased for many institutions. However, that tide could be shifting. J.D. Power recently released a report that predicted home equity lines of credit would double over the next 5 years as equity has exploded in many markets, and rates on fixed mortgages have become a little less attractive.

The J.D. Power 2018 U.S. Home Equity Line of Credit Satisfaction Study went on to note that the way in which HELOCs are delivered to members will change. So is your credit union ready? Consider the following:

- Over half of the Millennial survey respondents researched HELOCs through a digital channel. Does your credit union have a compelling story to tell about your HELOC products and services through the digital channel? How much can the member accomplish before they have to pick up the phone or walk into a branch?

- How does your team and marketing message clearly articulate why the consumer should choose your HELOC versus the numerous other options they are likely to have? The survey noted that 80% of Millennials shopped around at more than one lender.

- The study noted that nearly 64% of people looking for a HELOC have some sort of concern about the product, with the Millennials having the highest concern (at 87%). Some of the concerns include the variable nature of the loan or overextending themselves. How can you address those member concerns and help them feel confident about the structure of the product, and how they can use it effectively and efficiently? Are there training gaps with your lenders and front line staff?

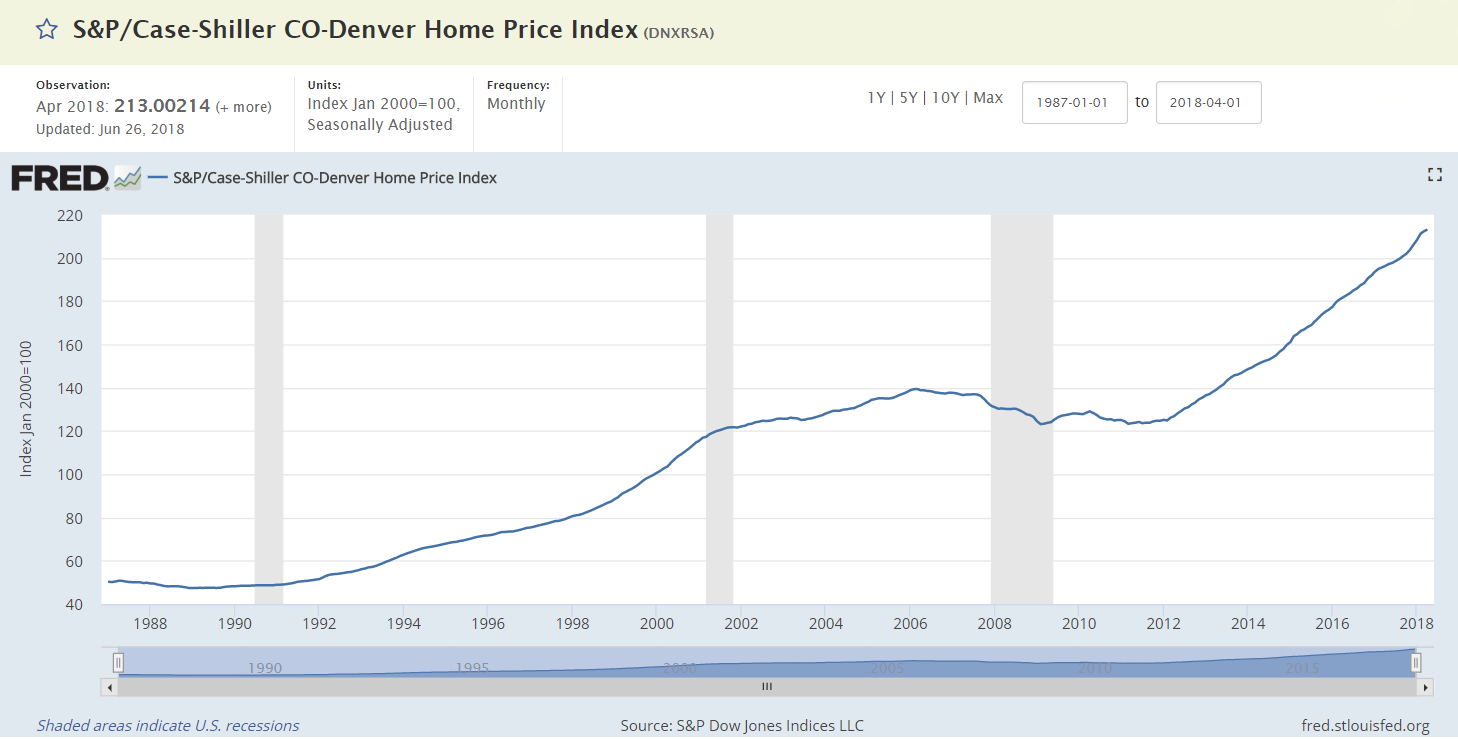

- Have you discussed and agreed upon your credit union’s risk appetite given what is happening in your markets? Consider the S&P/Case-Shiller CO-Denver Home Price Index graph below showing how home prices in Denver, Colorado have changed over the last 8 years. Financial institutions in the Denver area might look at underwriting a bit differently – perhaps taking less risk – than credit unions in markets who have not seen the same kinds of increases in home values.

- What are some of the credit risks? There is potential risk from a collateral perspective but also from a rising payment perspective. Will you underwrite variable-rate loans like a HELOC to help ensure that the member can cover the payment even if market rates continue to change? And if so, through what changes in the rate environment?

- How would growth in variable-rate HELOCs impact your financial structure and A/LM position? What stress tests should your modeling include? Common scenarios could include increasing provision for loan loss, or modeling with a periodic or lifetime cap that is lower than what is contractual.

- How would growth in HELOCs impact the credit union’s liquidity position from an unfunded member commitments perspective?

- CECL can be impacted by the unfunded portion of a HELOC, depending on how the loan is structured. Understanding the impact this could have in advance of any growth initiative would be important.

- Finally, don’t forget rates can now go down too! A couple of years ago, the common thought was that rates can only go up, but that is not the case anymore.

What other questions should your credit union be asking? The possibility of growing HELOCs again is an exciting prospect for many institutions, but there are many variables beyond rate to consider. Credit unions with a well-defined strategy and plan will be better positioned to take advantage of this potential opportunity.