Strategic Thinking for an Agile ALCO

October 16, 2019

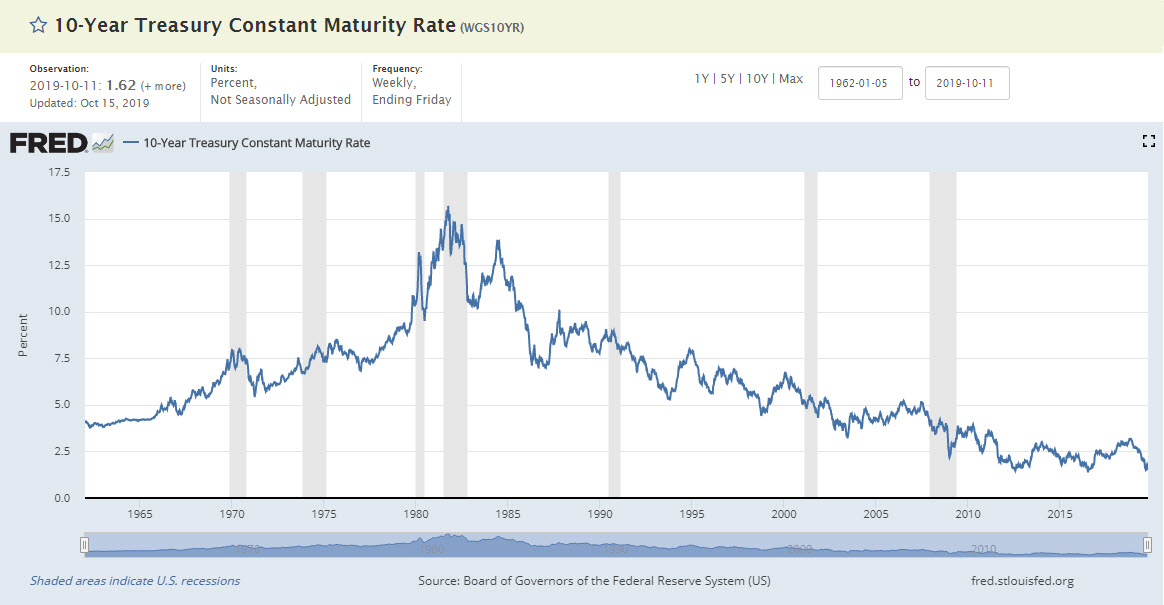

Continued uncertainty around the level and direction of interest rates seems to be the name of the game these days. A year ago, around this time, many market watchers believed that interest rates would continue to rise over the course of 2019. The exact opposite occurred, and since the Fall of 2018, long-term rates have decreased well over 100 bps, and the Fed has continued to reduce the overnight target rate. While there is no certainty that rates will continue to decrease, it would be a good strategic exercise for an ALCO to think through the possible implications to their financial structure if interest rates continue to head down.

From 2009 through 2016, short-term treasuries rounded down to essentially zero. However, long-term rates never dipped much below 1.5%. Imagine being in a scenario where both short and long-term market rates are at zero. This would represent an unprecedented rate environment in U.S. markets.

Have your team work to answer important business questions, so that if this future were to become reality you have already thought through some of these potential impacts, and will be more prepared to move forward decisively. Questions could include:

- How would the institution respond to rates going down? What might consumers be needing or wanting in this environment?

- How might competition evolve?

- How could this rate environment impact new volume rates on loans and investments, and ultimately profitability? Remember that the largest source of institution income traditionally comes from the net interest margin.

- Is there room to lower cost of funds in any material way? If not, then what other levers could you pull?

- Could you take on more credit risk? Do you have the expertise, products, and infrastructure to make higher risk lending profitable?

- If you decided to increase risk, could key stakeholders reach consensus on what an appropriate level would be? Achieving consensus on the potential impact to ROA and net worth is critical.

- Would this kind of rate environment necessitate changes to other strategic initiatives?

- Does your ALCO understand the profitability of different assets? If so, how are you using that information today, and how would it be relevant if rates dropped further? If not, what would you need to put into place to have access to that kind of information?

- Mortgage demand could increase materially in this kind of rate environment. Does your institution have the infrastructure in place to meet that demand and the channels to sell mortgage production if deemed necessary?

- If your margin is reduced materially, would you need to shift your business model to stay relevant?

- If rates continue to decrease, is there a situation where you might consider paying zero on deposits, or even going a step further and charging members a fee to keep money on deposit?

- Could a prolonged rate environment like this cause you to change your decisions on how you invest in the credit union’s future? Expensive strategic initiatives combined with low margin new business could materially reduce earnings. Now, for many places, this could be okay as long as stakeholders are comfortable with the timing and the source of the pressure. Communication is key.

Now is a good time to challenge conventional thinking and to look carefully at your business practices. The rate environments described above may never materialize, but walking through the exercise will have you better prepared for unexpected events and help create a more strategic and agile ALCO.