Mergers have become a fixture in the credit union industry, with more than 160 taking place each year. They show up in nearly every strategic planning conversation, often framed as the answer to growth challenges or competitive pressures. It’s easy to see why: on the surface, combining forces seems like a straightforward way to gain scale and resources.

At the same time, recent headlines are a timely reminder that mergers can be complex, and outcomes are not always straightforward. When high-profile situations surface (especially those involving disagreement, uncertainty, or changing direction) it reinforces an important point for leaders: mergers are major decisions with real operational, governance, and execution risk, and they’re not a guaranteed “win” simply because they look good on paper.

But here’s the challenge: Many leaders believe that finding the “right merger partner” will solve their toughest problems. That mindset can create dependency and delay the hard work of strengthening the organization from within.

Our recent analysis suggests a different perspective. Mergers can be good, but they are not a guaranteed solution. In fact, the data shows that even large mergers don’t always deliver the expected results. Here, we’ll explore why mindset matters more than the merger itself, and what leaders can do today to position their credit unions for success, with or without a merger.

A Balanced Look at Why Mergers Get So Much Attention

Editor’s Note: We wrote this prior to the recent merger challenges coming to light between SDCCU and Cal Coast Credit Union. That experience provides another reminder of the many challenges that can emerge in a merger process, reinforcing the importance of approaching such a major decision with clarity, diligence, and realistic expectations.

Mergers have a way of capturing attention in strategic planning sessions. It’s easy to see why: the idea of joining forces with another institution promises scale, new resources, and (at least in theory) a faster path to solving persistent challenges. The conversation almost always turns to, “If we just find the right merger partner, we’ll be set.”

But the reality is often more nuanced. Most mergers in the credit union industry are small, with a median asset size of just $22 million — far less than what many leaders expect, and not always enough, by itself, to materially change the trajectory of a mid-market institution. There were 160 mergers last year… but the typical merger is modest, and may not move the needle in the way many hope.

That said, small mergers can absolutely be beneficial in the right context, especially when they open up new geographic reach, expand field-of-membership opportunities, add complementary capabilities, or enable the surviving credit union to better serve members and accelerate growth. The key is being clear-eyed about what a merger can realistically accomplish, and ensuring the strategy is rooted in disciplined execution.

The expectation that a merger will be transformative is widespread, yet the data and experience show that outcomes vary widely. The real risk is that organizations start chasing mergers as a shortcut, hoping for an external fix, instead of rolling up their sleeves and addressing the core business challenges that drive long-term success. It’s worth asking: Are we pursuing mergers to avoid challenges and tough decisions, or are we truly focused on strengthening our organization from within?

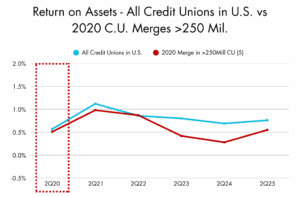

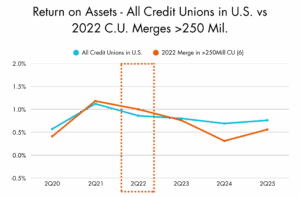

Earnings Outcomes From Material Mergers

Recent headlines are full of big mergers, where the future outcomes are not yet known. Historically, in the credit union industry, bringing in a merger greater than $250 million was considered a material deal, often expected to increase opportunities and strengthen performance. To pressure-test that assumption, we looked back at mergers of this size that were completed three, four, and five years ago, and checked in on their earnings performance post‑merger.

When we dig into the actual outcomes of these large, headline-making mergers, the story gets more nuanced. A quick analysis of mergers involving acquired institutions with $250 million or more in assets shows that a clear boost in earnings performance didn’t consistently materialize. Instead, the data revealed that these institutions often lagged behind the industry average in the years following the merger. In fact, some were performing well above average before the merger, only to fall below afterward.

*Source: Callahan & Associates

While the sample size is small (five material mergers in 2020, three in 2021, and six in 2022), the pattern still offers a helpful reminder: Even when the acquired institution is relatively large, improved performance isn’t automatic. That’s why leaders should approach mergers with clear eyes and realistic expectations, using them as a strategic lever (not a shortcut), and pairing them with the operational focus and internal work that ultimately drives results. The graphic is a reminder: mergers can be very good, but they’re not a sure thing.

The Power of Internal Strength

The most resilient organizations aren’t waiting for a merger to transform their future – they’re busy strengthening themselves from within. When leaders focus on solving their own business challenges, building operational momentum, and investing in their teams, they naturally become more attractive partners. The more you solve business challenges for yourself, the more that makes you a more attractive merger partner. Success tends to draw others in; people want to be part of organizations that are already thriving.

This principle shows up in leadership development, too. The emphasis isn’t on finding the perfect partner, but on becoming the kind of organization that others want to join. It’s about creating value, not just seeking it elsewhere. When a credit union builds its own strengths — whether through innovation, improved member service, or financial discipline — it positions itself for long-term success, with or without a merger on the horizon.

It’s worth asking: What are we doing today to strengthen our organization, regardless of merger prospects? The answer to that question is often the difference between waiting for opportunity and creating it.

A Mindset Shift: Don’t Wait, Create

A shift in mindset is essential for any leader navigating the merger conversation. The most effective approach is to focus on what can be controlled: building strength, driving progress, and creating momentum from within. There’s far more control over the outcome when the emphasis is on internal growth rather than relying on the hope that the perfect partner will appear.

The real question for leaders is this: Are we deferring progress by chasing a merger, or are we creating our own momentum? The answer will shape not just the outcome of any potential merger, but the future of the organization itself.