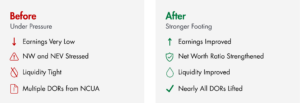

In less than a year, an approximately $1.5 billion Federal Credit Union materially improved its financial position. The Credit Union increased liquidity, improved earnings, and strengthened its net worth through a series of deliberate balance sheet actions, including loan sales, changes to funding, and cost reductions. Most of what was tested was executed as planned, and results showed up sooner than expected, with several key measures back within policy quickly. Regulatory follow-up reflected that progress, with nearly all Documents of Resolution lifted and the institution returning to good standing with the NCUA. The Credit Union ended the period on firmer footing, with a clearer path to maintaining stability going forward.

The Situation

The Credit Union ended 2024 in a tough position. They had very low earnings and their interest rate risk measures, Net Worth at Risk and NEV, were in a tough spot. The net worth ratio and liquidity were under pressure at the same time.

This was not a single-issue problem that could be solved by a simple fix (like addressing interest rate risk) alone. Examiners came in and issued multiple Documents of Resolution (DORs), including DORs tied to liquidity, interest rate risk, and the net worth ratio. The Credit Union had to address all of these simultaneously, which created real tradeoffs across the balance sheet. Actions that might help liquidity and interest rate risk could work against the net worth ratio or earnings, and vice versa.

Given the combined regulatory pressure and the need to make coordinated decisions across liquidity, interest rate risk, earnings, and capital, the Credit Union needed a structured way to evaluate balance sheet actions and their downstream impacts. They engaged c. myers to bring forecasting and scenario testing to these decisions, so the institution could understand the tradeoffs, determine what was viable, and move toward resolving the DORs while protecting the organization’s longer-term financial viability.

The Objective

The Credit Union wanted to remove the DORs and resolve the issues raised by examiners. Specifically, the institution needed a path that could simultaneously improve liquidity, reduce interest rate risk, and strengthen the net worth ratio. C. myers treated these as linked constraints and defined “success” as reaching a position where these measures were in a stronger position and examiner pressure was reduced. Beyond the immediate regulatory pressure, the Credit Union also needed confidence that the institution had long-term financial viability.

At the same time, the Credit Union needed to make hard balance sheet decisions without creating unacceptable losses. That meant evaluating actions like selling high-quality loans and managing the tradeoff between near-term earnings impact and improvements in risk and capital measures.

Our Approach

C. myers approached the engagement by turning forecasting into a practical decision‑making framework. With multiple pressures affecting liquidity, earnings, capital, and risk at the same time, the Credit Union needed a way to see how different actions would play out together over time. Rather than focusing on a single forecast or a narrow set of fixes, c. myers helped the team step back and evaluate the full range of options available to them.

The work centered on building and reviewing over 20 forward‑looking forecasts that mapped out different paths the institution could take over multiple years. Each path illustrated how various strategic choices would influence financial performance, risk measures, and regulatory outcomes. By comparing these alternatives side by side, c. myers helped the Credit Union clearly see the tradeoffs inherent in each option and understand which combinations of actions were viable and which were not.

As the analysis progressed, c. myers worked closely with management to narrow the field from many possibilities to a smaller set of realistic, executable strategies. The focus was not on producing technical models for their own sake, but on creating clear, board‑ready views of the future that could support confident decisions. By translating complex balance sheet dynamics into understandable outcomes across time, c. myers gave the Credit Union a roadmap that balanced near‑term improvement with long‑term sustainability and allowed leadership to move forward with clarity and conviction.

Impact

The work translated a complex set of competing constraints into a concrete path that the Credit Union could act on, and they moved faster than expected once the tradeoffs were clear. This showed up in execution speed, in the mix of actions they took, and in how quickly their position improved across liquidity, earnings, and policy alignment.

The Credit Union made meaningful balance sheet moves, including selling a large volume of loans, which materially increased liquidity. They also grew non-maturity deposits and allowed borrowings to pay down, which improved the overall funding and leverage position alongside the balance sheet changes. In combination, these actions helped their net worth ratio and helped their earnings.

The institution’s trajectory improved faster than anticipated, with “huge gains” already evident by mid-year versus earlier expectations tied to where they might land at the end of 2025. Management also made difficult operating expense decisions, which contributed to the improvement even though operating expense reductions were not heavily modeled. By September, their position continued to improve, with all DORs removed (except NEV risk) and a return to good standing with the NCUA.