Mortgages – A Few Things to Consider

November 17, 2021

|

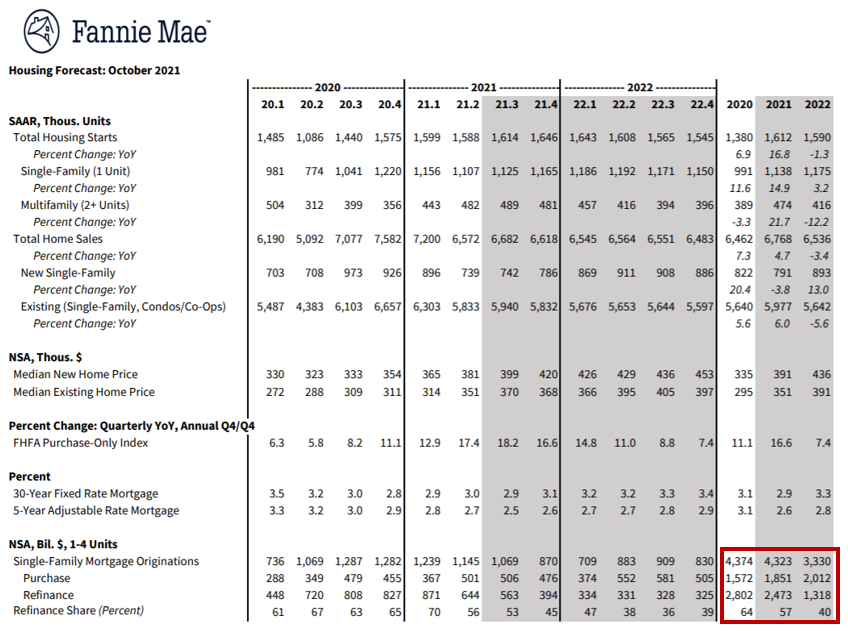

5 minute read – Where is the mortgage market headed? In 2021, the trend toward purchase money has become more prominent, but projections from FNMA would suggest this pattern could accelerate dramatically in 2022.

If Fannie Mae’s forecast is accurate, refis could decrease from 64% of originations in 2020, to 57% in 2021, slipping all the way down to 40% in 2022. So how well is your institution positioned to handle this shift? The following are a handful of considerations:

- Why should they choose you? What is your mortgage lending value proposition? If your rates and fees are competitive but the process is slow, what specifically needs to change, and when, to meet the demands of the purchase market? For example, how could you represent a preapproval for a member differently that helps them look stronger when competing for properties? Are you willing to commit to fast closing timelines or tout average close times that are better than average?

- Will they say it was easy? Buying a home should be fun, not stressful. But with the massive refi activity in recent years, many institutions have been completely overwhelmed and service levels have suffered on both refis and purchase mortgages. What changes need to be made to your processes and service delivery? When did you last review your internal and external service level agreements (SLAs) to ensure they are clearly articulated and understood by your team? How consistently are your SLA’s being met?

- What relationships do you need? For example, how important are relationships with realtors, brokers, and title companies to generate volume and live up to your SLAs? If those are a key part to your success, what can you do to win their business?

- How can your 3rd, 4th, and 5th party relationships affect your brand? If you are heavily reliant on vendors to deliver on your value proposition, how will you continuously assess and ensure they are delivering on their end, so your brand does not get damaged?

- What if refis remain strong? What do you need to do now to ensure you can continue to leverage refi opportunities while positioning your institution to be a key player in the purchase business? The possibility that refis can remain strong is supported by a survey conducted by Bankrate. The study suggested that 74% of homeowners who had a loan before the pandemic have yet to refinance as of July 2021.

- What about financial impact? From a budget and ALM perspective, make sure you are testing the impact of reduced mortgage volume, particularly if your institution is not as well positioned to compete on purchase mortgages. For example, how much revenue was generated on refis? What if a certain percentage of that goes away in 2022? What other revenue generating options should be explored if you are not positioned to make up the revenue in the purchase market?

- What about risk appetite? With the increase in home values seen in most markets, many refis were booked at relatively low LTVs. Purchase mortgages may be at materially higher Loan-to-Value (LTV). Should you change your criteria, such as requirements around Debt-to-Income (DTI), employment history, credit score or LTV?

- How ready are you if 2nd mortgages make a comeback? There could be more opportunity for 2nd mortgages, particularly if mortgage rates steadily increase and refis slow. Now is a good time to make sure your fixed and variable home equities are competitive and your institution is well positioned to deliver these products.

Revenue creation and relationship cultivation are key. If mortgages are a big strategic focus for your organization, don’t underestimate the value of investing time to continuously think critically about how to remain highly competitive in this quickly evolving market. Remember, the point at which you address an opportunity is directly related to the number of viable options you have to leverage.