4 minute read – A few months ago, we posted an investment strategy blog, touching on the importance of understanding risk versus return trade-offs when evaluating high-premium investments.

As investments carrying a premium continue to be evaluated, we thought it would be worthwhile to circle back, considering purchase premiums are not exclusive to the investments. As some teams wait for the lending machine to pick back up, participation loans are being explored and can often have similar premium risk.

What can make participation loans unique from investments is the potential for additional geographic risk. For example, are the mortgage loans being purchased located in an area that is seeing higher than normal displacement? There are certain pockets of the country experiencing faster mortgage prepayment than other areas. Similar to high-premium investments, make sure to test a wide range of prepayment speeds that capture a few of the realities of this new environment, such as:

- Mobile Workforce: A more mobile workforce that can perform their job from a remote location could cause faster prepayment and lower marginal ROA.

- Supply Shortages: In some markets, inventory of homes is very low. This could create less displacement, slower prepayments, and actually increase the yield of the participation loan.

- Diversification: Consider how many loans there are in the pool. In some cases, a pool could be comprised of jumbo loans, where one or two early payoffs can significantly impact performance of the participation loan.

While cash flow uncertainty has always played a role in determining when premium is expensed, faster and more volatile prepayment speeds have increased the importance of performing multiple prepayment tests when evaluating premium-related opportunities.

For example, consider evaluating the following participation loan with a premium at time of purchase. While every participation is unique, notice how in the example below, the marginal ROA experiences a wide range of change from barely break-even to close to 2%.

If you think the 30-40% prepayments from 2020 and a marginal ROA that is barely break-even will not happen, consider that the 10-year Treasury fell roughly 100bps during the past year, increased nearly 40bps in the past month, and still has plenty of room to decrease from its current level. Keep in mind that many other economies around the world have negative or near 0% debt yields and mortgage rates that are considerably lower than the U.S.

There is no way to know for certain what will happen to market interest rates and, ultimately, prepayment speeds. Therefore, it is important to help your team see the potential range of performance if prepayments were to dramatically increase or, conversely, dramatically decrease.

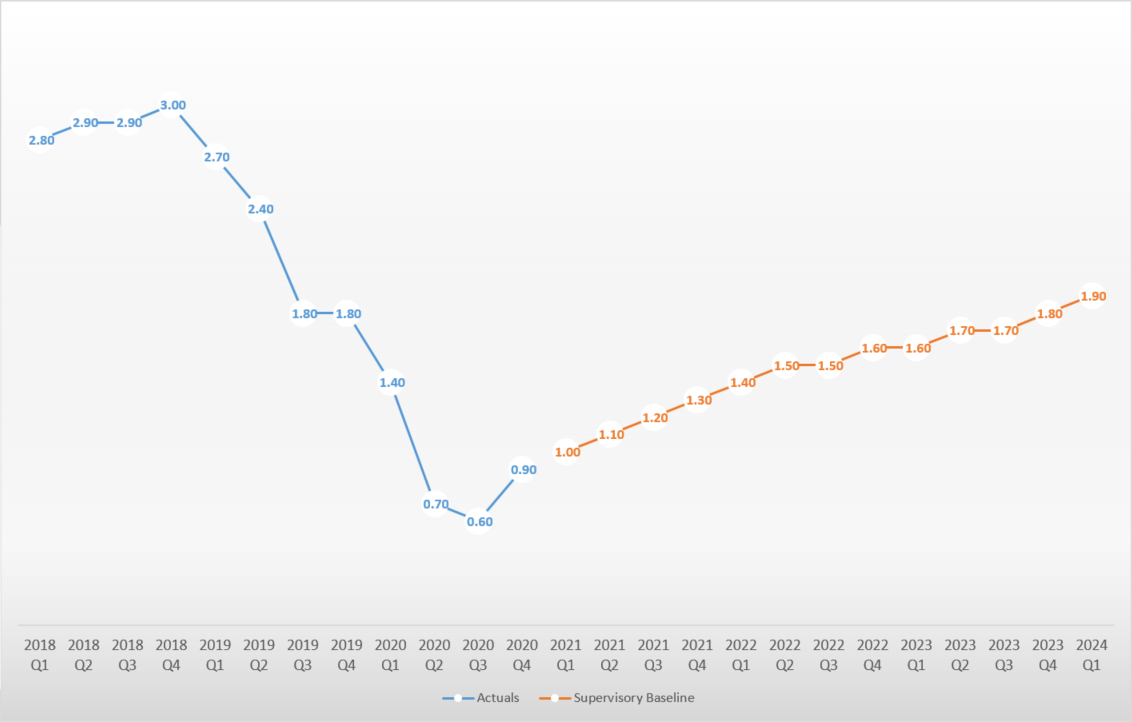

The orange line in the graph below details the Fed’s supervisory scenario baseline projection for the 10-year Treasury.

Sources:

Actuals: Federal Reserve

Forecasts: Federal Reserve

If the Fed projection of higher longer-term interest rates comes true, it is possible prepayment speeds decrease and opportunities like the one above experience a materially higher yield. High-premium participation and investment opportunities could provide some protection against rising market interest rates.

A case can be made for both higher and lower longer-term interest rates. The objective here is not to predict the direction of market interest rates. Instead, the goal is to encourage providing decision-makers with a range of potential outcomes, both good and bad, before ultimately taking action. The current rate environment and other unusual external forces pose unique risk versus return trade-offs that require careful consideration when strategically positioning the balance sheet.