4 minute read – Every day, leadership teams are evaluating what to do with all their liquidity. Discussions often include setting aside dollars for investment purchases, holding more mortgages, and being positioned to meet pent up consumer loan demand. But before plans are put into motion, help paint a picture for your team by using business intelligence that is right at your fingertips.

While there are many ways to prepare for deposit uncertainty, there is value in understanding how customers’ average deposit relationships have changed since pre-pandemic and what it could mean for the business going forward.

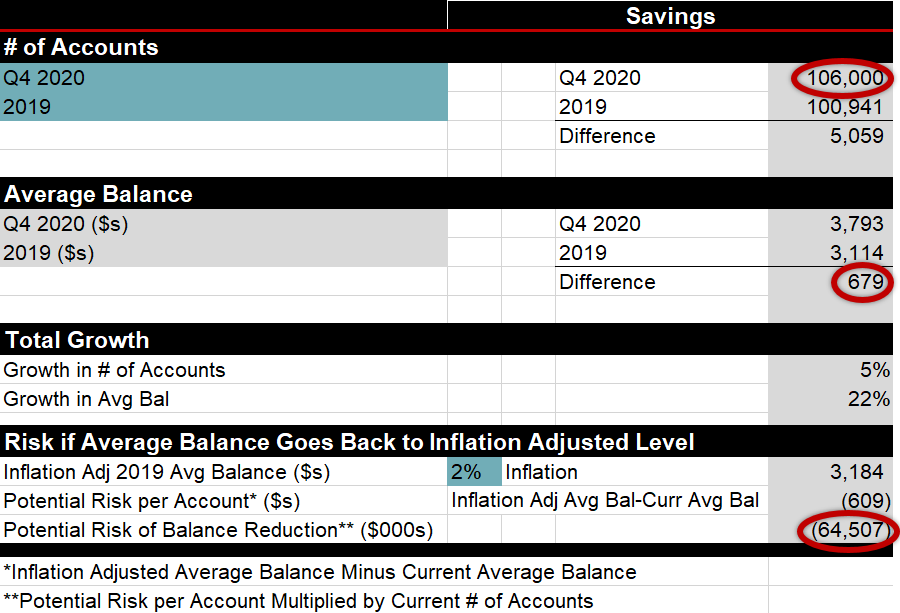

For example, consider a $1B institution that over the last 18 months has seen customers increase their savings account balance 22%, or roughly $680 on average. While an average balance increase of $680 does not seem like much, it can add up very quickly. If all account holders take their balances back down to pre-pandemic levels, after accounting for moderate inflation of 2% over this period of time, it could represent roughly $65M in deposit outflow.

It is important to acknowledge that there is no guarantee that some or all the deposit growth from the past 18 months will head back out the door, and impossible to predict if and when it could occur. While uncertainty remains, this type of business intelligence can enhance the quality of liquidity discussions and contingency funding plans. Keep in mind, if deposits are going out the door, perhaps spending is increasing, and it may be a great opportunity to generate loan growth.

Applying the same logic from savings to both checking and money markets, the combined outflow, adjusted for inflation, is $143M or 14% of assets for the $1B institution. This assumes 100% of savings, checking, and money market accounts decrease account balances to pre-pandemic levels from 2019.

Having this type of business intelligence readily available can not only help inform liquidity stress tests and contingency funding plans, but can also be used for interest rate risk analysis. Consider how +300bp earnings, net worth/capital, and EVE/NEV ratios are currently being impacted by record levels of cash. This type of analysis can help answer important questions, such as, what do the ALM results look like with a shrinking balance sheet, less deposits, and less cash? and how might the structure need to change in order to fund new loan growth opportunities as deposits are leaving?

Future customer behavior is unknown. For some, the pandemic may have caused a permanent change in behavior, resulting in a higher savings rate going forward. As a result, there is no guarantee average balances will come back down or deposits will head back out the door. But as strategic discussions are taking place and large amounts of liquidity are being set aside for investments and future loan demand, it’s important to consider how your average deposit relationships have changed and what it could mean for your institution.