NCUA – Rethinking NEV

July 6, 2016

It’s no secret that the NCUA is planning to implement new guidance for net economic value (NEV) testing this year.

From NCUA’s recent open meeting, some key elements of the new guidance include:

- Non-maturity deposit (NMD) values will be capped at a premium, not to exceed 1% in the current rate environment.

- NMD benefit will not exceed 4% in a +300 bp rate environment.

- NMD guidelines may need to be re-calibrated over time.

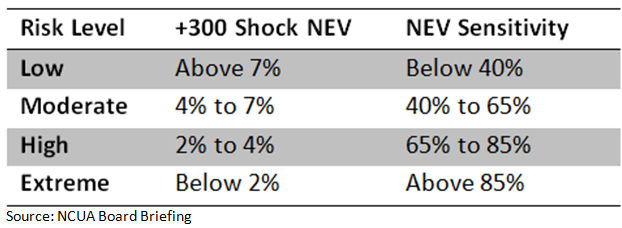

- Risk thresholds:

The new test is being designed to support the NCUA’s responsibility with respect to understanding risks to the insurance fund, and is intended to create greater comparability between credit unions. Credit unions will still be expected to run their own A/LM analyses, to understand risks to earnings and net worth, and support their internal risk management and decision-making.

Having modeled thousands of NEV simulations, NMD values are arguably the most significant wildcard. For most of our clients, we already model at least two views of NEV: one using their base case assumptions for NMDs and another showing shares at par. Historically, NEV with shares at par was used by examiners to get the same comparability concept, and to limit the variety of deposit assumptions.

Shares at par ascribes no market value to the shares, thereby removing any benefit of low cost deposits from the analysis. The new guidance then, at least with respect to shares at par, would be some improvement. Keep in mind, though, that any standardization of deposit values would hide any material differences in deposit pricing between credit unions.

However, no matter how much rethinking of NEV occurs…

…NEV, even with standardized assumptions, is still not going to address fundamental business issues. For example:

- NEV doesn’t recognize the different earnings contributions and the risk/return trade-offs that exist between assets.

- Overnight investments earning 0.50% devalue less and perform better in NEV than a fixed-rate loan yielding 4.00%. It’s important to note that the loan contributes greater revenue in the current rate environment, as well as in a +300 bp rate environment.

- A $10 million purchase of a new headquarters would not show any hurt to NEV results because the asset would not devalue as rates increase, but it would have an impact on earnings over a very long-term horizon.

- Moving from mortgages to autos would reduce NEV volatility in a rising rate environment, but NEV would not show you the possible reduction in earnings power.

- The standardized assumptions still do not distinguish between pricing for share drafts, regular shares, and money markets. Therefore, a credit union could pay 1 bp on all NMDs or 100 bps, and the NEV results would not be different. But of course, the earnings would be drastically different.

- NEV won’t tell you if you’re making or losing money. The previous bullet is a great example of this fact. For this reason and many more, NEV won’t show you risks to profitability and if the decisions you’ve made, or are considering will cause your net worth to fall below Well Capitalized.

To sum it up, NCUA has a new test. Passing NCUA’s test does not replace the need to understand short- and long-term profitability, risks to profitability, and risks to net worth. Understanding and managing these risks are directly related to creating a relevant and sustainable business model.