When Risk Limits and Business Decisions Collide

June 12, 2019

There is a lot of uncertainty these days in the economic and interest rate environments. This has made decision-making at credit unions more difficult. In January 2019, we wrote a blog on some ways to manage through an environment with a flattening yield curve.

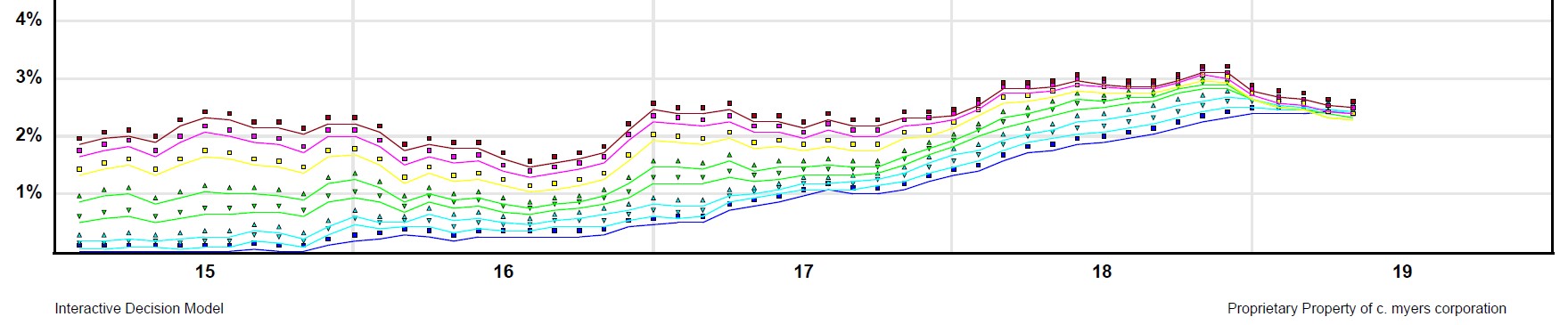

Since that time, the yield curve has not only flattened, but at various times throughout the first half of 2019 we have seen inversions between short-term Treasury rates and long-term Treasury rates as longer-term rates have steadily fallen. A flat or inverted yield curve is often a predictor of falling rates in the future, as well as an economic slowdown.

Historical Government Interest Rates

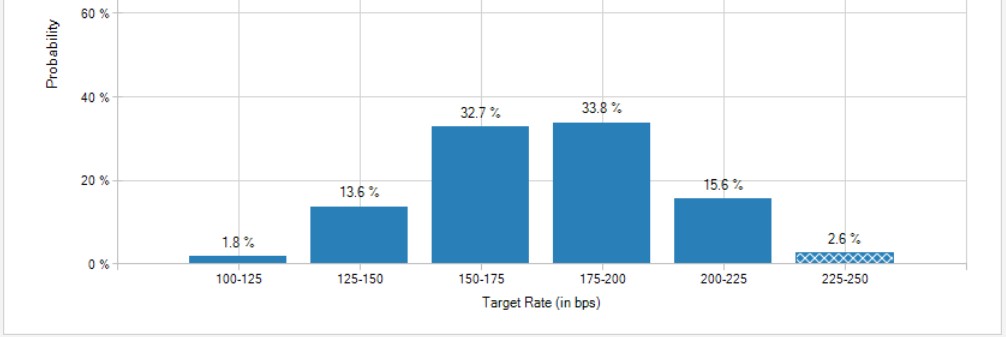

Fed Funds futures in recent months have painted a similar picture, with a bulk of the bets on the side that short-term rates will decrease over the course of 2019. Fed Funds futures are pointing toward a lower Fed Funds rate by the end of 2019.

Target Rate Probabilities for 11 Dec 2019 Fed Meeting

With market rates being in flux now, it is easy to forget that short-term market rates have increased more than 200 bps since the end of 2015. This has made the interest rate risk tests and policy compliance tougher.

This has created a situation where some credit unions are bumping up against policy limits if rates were to rise, while desiring to make balance sheet adjustments that could help support earnings if rates decrease.

This has put some credit unions in a collision course between policy pressures and shoring up earnings today. The reality is that many (but not all) balance sheet decisions that support earnings in a down rate environment are going to add risk as rates rise.

Consider a credit union looking to move funds into longer-term fixed rate assets such as term investments or mortgages, to prepare for the possibility of lower rates. In this example, a credit union with about $750M in assets and $80M in overnights is evaluating moving $50M from overnight funds into 5-year investment CDs. While shifting funds from overnights to term investments would help earnings 2 bps today (and more if rates decrease), this credit union would be very close to being outside of its 6% net worth policy limit in a +400 bps rate environment (middle top window) and to its 50% NEV volatility limit (top right window).

The average ROA on existing commitments would be 9 bps higher implementing the Investment CD strategy if market rates returned to where they were in 2015 when short-term market rates were about 200 bps lower than they are today.

This is not to suggest that the only way to improve earnings today is to take more interest rate risk in a rising rate environment. However, many of the most readily available levers could have that impact, such as adding longer-term loans or investments, shortening liabilities, or shifting more of the balance sheet into fixed rate assets.

This is where having an agile ALCO comes in. ALCOs who have deliberate and ongoing discussions about balancing business decisions and risk limits are more likely to navigate the uncertainty without having to compromise their overall risk tolerance. They acknowledge that changing policy limits is not the first line of defense. Frequent quality discussions and documentation of rationale are two critical components of agile ALCOs.

Another critical component is for decision-makers to stretch their thinking. What are other options the credit union could consider that would help insulate earnings in the down environments, while not adding material risk if rates were to increase? Think beyond just the balance sheet structure, but consider all five components of ROA, including net operating expenses. For example, ensure newly originated loans are priced right, or put more focus on creating operational efficiencies. Both steps could produce higher earnings regardless of where rates go.